As we navigate ongoing market volatility – most visibly reflected in the daily price swings of stocks and bonds – we believe it is important to highlight how we are approaching private investments in this environment. While private investments are valued less frequently and may appear less volatile, they are subject to the same macroeconomic forces that drive public markets and their valuations often move in the same direction, just with a lag.

Private investments are generally more difficult to “time” than public markets due to their illiquidity and the long duration over which capital is deployed and returned. This reinforces the importance of maintaining a disciplined approach – methodically committing capital to high-quality, top quartile managers with the expertise to strategically deploy capital, actively create value, and return it over a full market cycle.

To help inform our approach, we examined the performance of private equity buyout funds that began investing before (2004-2006 vintage), during (2007-2008 vintage) and after (2009-2010 vintage) the Global Financial Crisis (GFC), focusing on returns in both absolute terms and relative to the S&P 500. Please note that we completed this analysis on other private asset classes such as private credit and real assets as well and reached similar conclusions.

Absolute Performance

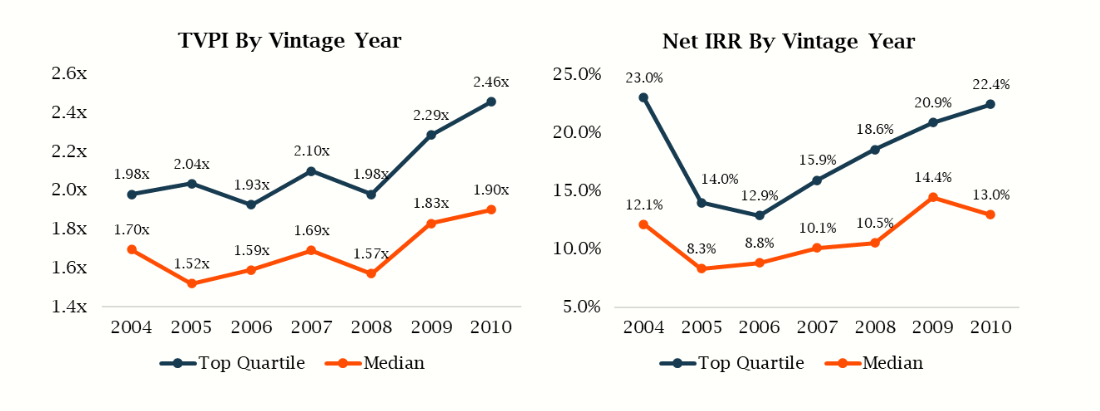

Below is the top quartile and median performance of all private equity buyout funds by vintage year from 2004 to 2010. TVPI (Total Value to Paid-In) measures the total return on a cash-on-cash basis while net IRR (Internal Rate of Return) represents the annualized return, accounting for the timing of cash flows, net of fees.

Source: Burgiss

Key Takeaways

- Private equity buyout funds delivered strong absolute performance across all vintages through the Global Financial Crisis (GFC), with top quartile funds generating 1.9x–2.5x TVPI and 12%+ net IRRs, and median funds returning 1.5x–2.0x TVPI with 8%+ net IRRs.

- While the 2004–2008 vintages ultimately returned similar levels of capital (as shown by comparable TVPIs), the 2005 and 2006 vintages exhibited lower net IRRs, suggesting it took longer to realize those returns. These funds likely held their assets longer as they navigated a more challenging exit environment, particularly due to a slowdown in mergers and acquisitions (M&A) activity during and after the GFC.

- Investors who continued to commit capital through the GFC captured outsized returns, as the 2009 and 2010 vintages produced the strongest absolute performance. These funds likely were able to buy assets at lower valuations and sell them into a strengthening M&A environment.

Relative Performance

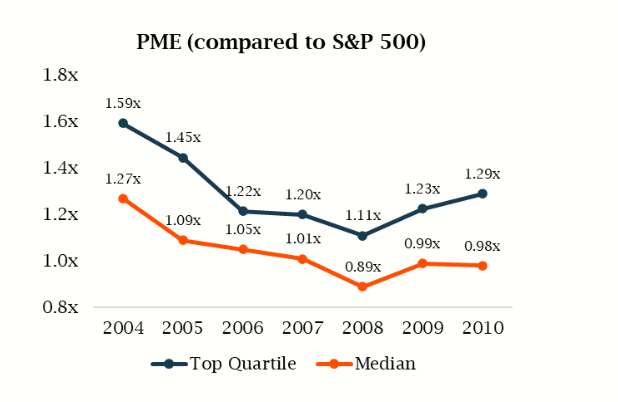

We examined the performance of private equity buyout funds relative to the S&P 500 using the Public Market Equivalent (PME), a metric that compares the return of a private investment to what would have been achieved had the same cash flows been invested in a public index. For example, a PME of 1.25x means the private investment outperformed the public market equivalent by 25% over the life of the investment.

Source: Burgiss

Key Takeaways

- Top quartile buyout funds outperformed the S&P 500 in every vintage year, with 2008 generating the lowest outperformance at 1.11x and 2004 achieving the highest at 1.59x.

- 2005 was the second-worst vintage by net IRR but was the second-best on a relative basis. These funds returned the bulk of capital between 2011–2014, when public equities were still recovering from their 2007 highs. Though they “only” produced a 14% net IRR, they accomplished it in a challenging period for public equities.

- Manager selection was key: Across all vintages, top-quartile funds delivered consistent outperformance, while median managers largely tracked the index.

While private investments are not immune to market volatility or macroeconomic stress, they can represent a valuable allocation in client portfolios – particularly when accessed through top-tier managers. We continue to take a disciplined approach, methodically committing capital to high-quality, top-quartile managers who deploy capital strategically, drive value creation, and return capital over a full market cycle.

Disclosure

Heritage Wealth Advisors is an SEC-registered investment advisor. This article does not constitute an offer to sell any securities or constitute a solicitation of an offer to purchase such securities. This article should not be used as the sole basis for making a decision to invest with Heritage. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Past performance is no guarantee of future results.